11 Mar Finding the best approach to portfolio modeling

Portfolio managers (PMs) have an important responsibility when managing their clients’ assets. Understanding a client’s goals and unique needs, and maintaining a meaningful relationship, are always a top priority. The execution of key portfolio decisions – either across hundreds of portfolios or for a single client – must be efficient and effective. Portfolio modeling and rebalancing tools in Croesus provide PMs with this key capability.

Leveraging a robust set of modeling and rebalancing tools is crucial for PMs so that they can grow their practice and optimize how client portfolios are managed. Portfolio modeling and rebalancing tools in Croesus offer this key capability, while providing the much-needed flexibility the industry now demands. Is it best to model at the account or household level? What are the benefits of using a single model, a model of models, or sleeves? Depending on the PM’s perspective, the tools can be used differently to support the majority of client scenarios.

Degree of portfolio customization

Generally speaking, a higher degree of customization and variety will mean more models to manage and more effort to monitor and rebalance investments. In the case, however, in which a book is composed of clients who differ primarily based on risk profile and life stage, a high degree of customization is not necessary.

Each PM must ultimately decide if custom portfolios are the most important part of their value proposition. For a book containing ultra-high net worth clients, it may be entirely reasonable to build custom portfolios that reference unique needs, tastes, and tax structures. In this scenario, the “model by sleeves” structure can be used to manage the unique needs of clients and still provide the PM with scalability. An alternative to this approach would be attaching custom models to a household.

Most PMs using Croesus modeling expect a tool that supports mass rebalancing scenarios, and they use the system features (such as restrictions and locked positions) to achieve moderate customization when necessary. Both the model of models and the sleeve function can achieve this efficiently.

In a common scenario, a PM could manage a core set of models (such as Canadian equity, US/international equity, fixed income, and alternative investments). These models would be combined in different proportions in a “container” called a model of models. Client portfolios would be assigned to the model of models that best suits their risk profile and goals, providing consistency to the book of business’s underlying models.

Asset placement

The simplest way to manage a single model is at the account level. In addition to being the most straightforward setup, this can be efficient for small-to-medium-sized accounts and scenarios, where tax efficiency (and therefore asset placement) has little value. An example of this is the client who only has registered assets across one or two accounts, with a single goal of retirement.

A PM could create a handful of models with differing asset allocations (30% equity/70% fixed income, 50/50, 70/30, and so on) and attach them to accounts based on best fit. A client with two accounts (both attached to the same balanced model) will effectively have identical holdings in each account. Some PMs prefer this straightforward approach, which nevertheless has its own shortcomings.

By contrast, a tax-efficient approach would prescribe that fixed income assets be held in tax-deferred accounts (RRSPs, TFSAs), while tax-friendlier, dividend-paying growth securities are held in the non-registered account. Similarly, there is a benefit to the client holding US assets to have these assets settle and receive income in the currency of the security, avoiding unnecessary foreign exchange spreads. To achieve these benefits, the “identical account” approach described above is not possible. Either assets must be placed in certain account types manually, or a series of system rules (rebalancing criteria) can be used to maximize the impact of these strategies.

Managing a portfolio at the client or household level (via a group of accounts) and using the smart rebalancing criteria to determine asset placement, can achieve many of these benefits in addition to reducing unnecessary trading volume.

Oversight and monitoring

In addition to rebalancing, Croesus allows PMs to actively monitor assets in a portfolio, alerting to scenarios where asset allocation exceeds tolerances.

PMs present their approach to the client in the form of an investment policy statement (IPS) that describes the assets in the context of the client or household. The benefit of modeling to this same portfolio construct (client or household) is that you can both rebalance and proactively monitor the assets in the same way.

If a PM’s preference, however, is to align to KYC (know your customer) and the dealer statement, they might prefer to model at the account level, allowing them to maintain traceability.

Rebalancing process

One important feature of using models of models, or sleeves, is the ability to attach multiple models to a single portfolio. This allows a PM to rebalance each model independently without having to rebalance entire portfolios. For example, one can have hundreds of portfolios or accounts attached to three models in different proportions. In the case where the three models are Canadian equity, foreign equity, and fixed income, and a change is required in the Canadian equity model, that model can be rebalanced without unnecessarily impacting the others.

When rebalancing accounts, there are many rules to keep track of, and any mass execution of large trade volumes requires a well-managed process. The more complexity and features are introduced to the process, the more a detailed understanding of the tool and the algorithm being used is required. To take advantage of all the possible features, the person executing (the PM or the sales support team) must be well informed about the system and validation best practices.

Additional insights

Regardless of the PM’s preferences and approach, Croesus allows exceptions to be handled without the need to create custom portfolios or manage dozens of models:

- Need extra liquidity for registered retirement investment fund (RRIF) withdrawals or a major purchase? Use the cash management function.

- The client has unique assets they can’t sell? Lock the position and/or create a substitute security.

- Unsavory news on a stock? Use the replace feature to sell all (or part) of the investment and replace it with another investment in equal proportions.

- Need to maintain a cash reserve for management fees? Use the reserves feature related to cash management functionality.

Get more with Croesus

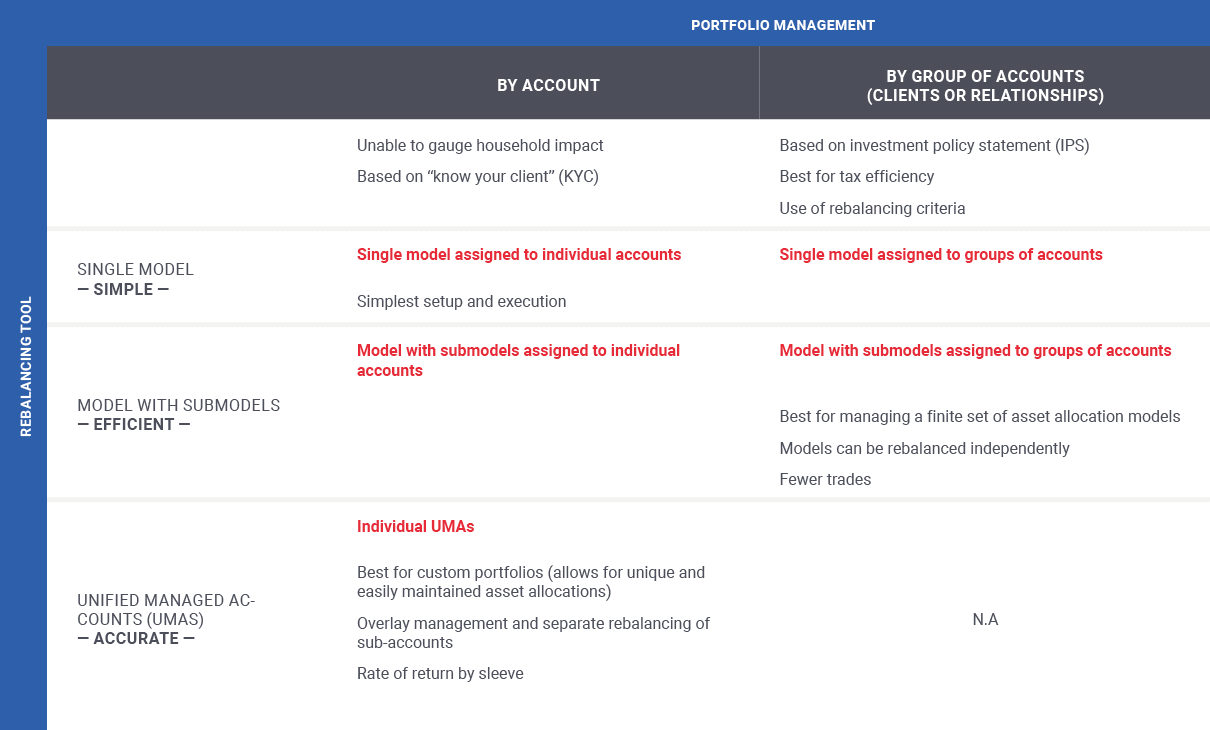

Croesus offers a variety of tools to manage models, rebalancing, and portfolio composition. Below is a quick reference guide that illustrates some of the different tools and approaches, and the pros and cons based on the criteria discussed in this article.